Level four.

Fourteen months ago, these two words meant nothing to me. But for the past year, they have defined me.

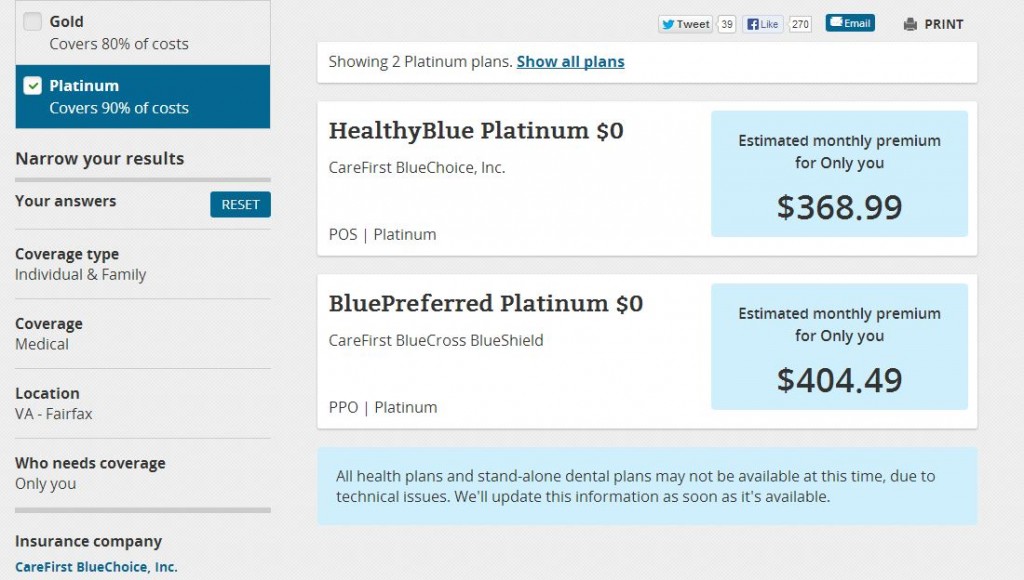

Level four is the rate at which I am approved for health insurance premiums. That’s on a scale from one – four. Think:

1.Health-obsessed Chris Traeger (Parks and Recreation)

to

4. Terminally ill Walter White (Breaking Bad).

Considering I don’t fall under either of these extremes, I anticipated receiving a level three rating. When the insurance company informed me I could be insured at a level four rate or not at all, I vacillated between unadulterated rage and numb defeat.

While my friends were buying cars, apartments and engagement rings, I was dealing with the reality that at 26 years old, I was facing health insurance premiums that would demand more than half my take-home pay. As someone who has an autoimmune condition, living without health insurance – even for one day – isn’t an option for me. So I’ve remained in the nest a little longer than either my parents or I ever anticipated.

Despite the fact I’m not where most people would imagine their lives being at age 27, I still consider myself to be incredibly lucky. In fact, lucky doesn’t even begin to describe how fortunate I am to have two remarkably supportive parents. Do I wish I were writing this piece from a studio apartment rather than from my childhood bedroom, where I still reside? Sure. But my parents’ unwavering support means I’ve never had to struggle because of my health. For that I am eternally grateful.

The other side of the coin is that while I’ve never struggled financially, I’ve never been able to live independently, either. Independence is a luxury I simply can’t afford.

I frequently hear pundits argue about how detrimental the Affordable Care Act (“Obamacare”) is to my generation. I respectfully disagree.

Yes, I have a major self-interest in the successful implementation of this hotly-contested provision of Obamacare, which will prohibit insurance companies from charging higher premiums for people with pre-existing conditions. That much is obvious.

But take a moment to consider it from my perspective. To increase a young, healthy person’s individual premiums $100-$200 is an inconvenience. To put it bluntly, it sucks. But to reduce a young, chronically-ill person’s premiums $500-$1000 is nothing short of life-changing.

To say Obamacare will change my life is not hyperbole. I will still be paying more than most people who don’t require “platinum” coverage, but I am looking at a 70% drop in my monthly premiums.

That said, by no means do I think the law is perfect, nor do I discount anyone’s frustrations with Obamacare’s oft unintelligible complexities. Given the sheer volume and intensity in which so many are speaking out against Obamacare’s negative consequences, I simply wanted to lend my voice, however small it may be, to the other side of the argument.

I admit, there’s no real way to put a positive spin on the Healthcare.gov rollout. Even people who were previously in support of Obamacare are becoming jaded by the calamitous process. Perhaps some are worried the fragile system will simply collapse, while others are annoyed that their premiums are about to double or triple overnight.

If you are in the latter category, I envy you.

I envy your dissatisfaction about rising health care costs. Your frustration over higher premiums means your life doesn’t currently – nor likely has it ever – revolved around doctors’ visits. It means you’ve never had the realization that you must choose between rent or health insurance, because you can’t afford to pay for both. It means you’ve never had to make a career decision based upon health, rather than aspirations or dreams.

Obamacare means something very different to me. It means that for the first time in my adult life, my health will no longer define me.

That, in and of itself, is priceless.